Twitter Timeline

FourByThree proposes the development of a new generation of modular industrial robotic solutions that are suitable for efficient task execution in collaboration with humans in a safe way and are easy to use and program by the factory workers.

The project was active for three years, December 2014-2017.

−

Source: The Machinist

Are first being used to help workers fit shock absorbers to Fiesta cars.

More than 100 years after the first cars rolled off Henry Ford’s pioneering assembly line, Ford Motor Company is breaking new ground in the way workers and robots are collaborating to manufacture vehicles.

New collaborative robots, also known as co-bots, are first being used to help workers fit shock absorbers to Fiesta cars, a task that requires pinpoint accuracy, strength, and a high level of dexterity. Employees work hand-in-hand with the robots to ensure a perfect fit every time.

The trial at Ford’s assembly plant in Cologne, Germany, is part of the company’s investigations into Industry 4.0, a term coined to describe a fourth industrial revolution, embracing automation, data exchange and manufacturing technologies. Ford sought feedback from more than 1,000 production line workers to identify tasks for which the new robots would best be suited.

“Robots are helping make tasks easier, safer and quicker, complementing our employees with abilities that open up unlimited worlds of production and design for new Ford models,” said Karl Anton, director, vehicle operations, Ford of Europe.

Measuring a little more than 3 feet high, the new robots work hand-in-hand with the line workers at two work stations. Rather than manipulate a heavy shock absorber and installation tool, workers can now use the robot to lift and automatically position the shock absorber into the wheel arch, before pushing a button to complete installation.

“Working overhead with heavy air-powered tools is a tough job that requires strength, stamina, and accuracy. The robot is a real help,” said Ngali Bongongo, a production worker at Ford’s Cologne plant.

Equipped with high-tech sensors, the co-bots stop immediately if they detect an arm or even a finger in their path, ensuring worker safety. Similar technology also is used in the pharmaceutical and electronics industries. Developed over two years, the robot program was carried out in close partnership with German robot manufacturer, KUKA Roboter GmbH.

Ford is now reviewing further use of collaborative robots that can be programmed to perform tasks ranging from shaking “hands” to making a coffee.

“We are proud to show the capabilities of our new generation of sensitive robots that are supporting and collaborating with Ford workers by carrying out ergonomically difficult and technically challenging tasks,” said Klaus Link, key account manager, Ford, KUKA Roboter GmbH. “As part of our close partnership with Ford and based on the feedback from employees, we are looking forward to further challenges.”

Source: Robotic Industries Association (RIA)

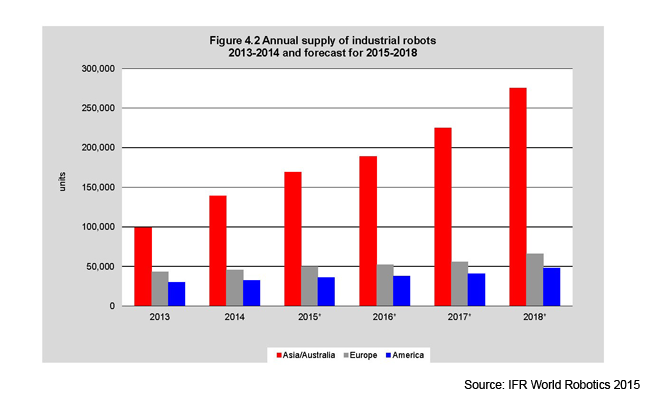

Once again, the robotics industry broke its own record. In 2015, worldwide industrial robot sales rose by 8 percent, surpassing for the first time 240,000 units globally, according to the International Federation of Robotics (IFR). For the third year in a row, robots sales are at an all-time high. By 2018, the IFR estimates that 2.3 million industrial robots will be in operation across the globe.

It’s a global race against rising labor costs, an aging workforce, and greater demands for productivity and quality. It means exponential technological advances and easier access to lower-cost technologies. It’s a boon for venture capital investing, corporate research spending, and government funding. It’s a shift from specialized markets to broader industries and applications. For many manufacturers, it’s become a do or die scenario.

This is the business of automation. It’s fast and furious. Hold on tight.

Come along as we dive into the statistics, and survey robotics analysts and industry veterans for a closer look. Depending on who you ask, the “big news” in automation and robotics varies from AI and the Internet of Things, to human-robot collaboration, and even commercial drones. But our contributors agree on one area in particular. All eyes are on China.

China on the Cusp

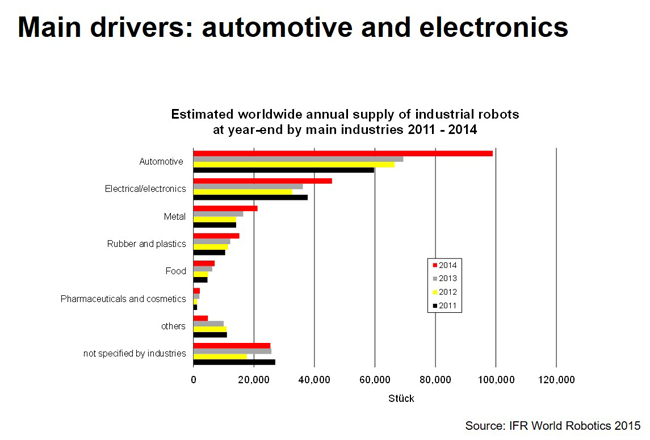

The IFR estimates that between 2015 and 2018 about 1.3 million new industrial robots will be installed in factories around the world. Asia will continue to dominate the ramp-up, with China the primary contributor. Meanwhile, Europe will continue to inch out North America for robot installations. Automotive and electronics are still the top industry sectors for robotics use.

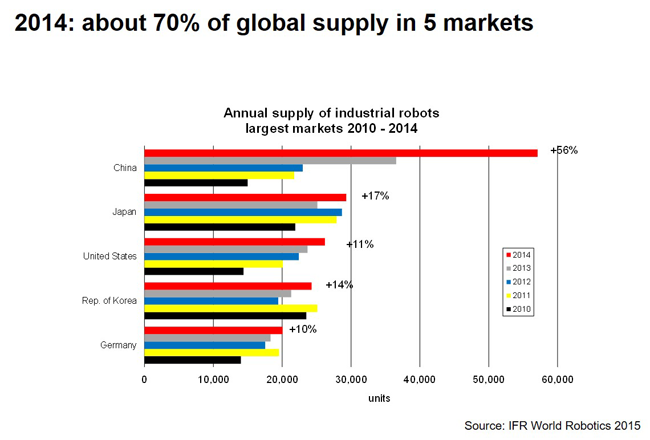

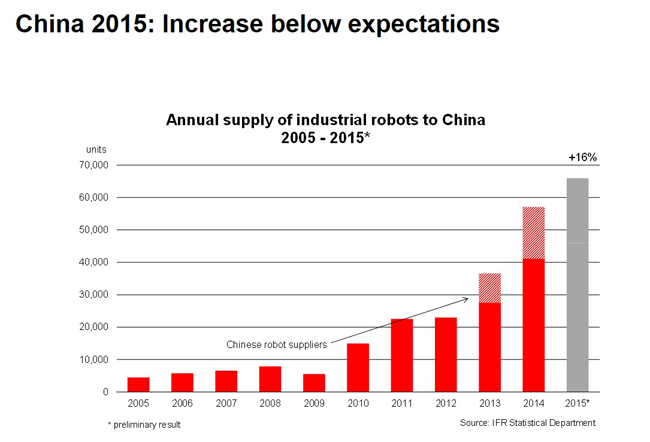

Across all global markets, China is number one for robot sales. In 2013, China surpassed Japan as host to the largest annual supply of industrial robots. Just a year later, China had a 56 percent increase, blowing away the other top markets for robots – Japan, U.S., Korea and Germany.

Joe Gemma, President & CEO of KUKA Robotics Corporation in Shelby Township, Michigan, is IFR’s newly elected President. He says demands for higher productivity, tighter tolerances, mass customization, miniaturization, and shorter product life cycles are driving double-digit growth for robotics worldwide. Particularly in China, where robot sales rose by 16 percent in 2015.

“The automotive industry and the electronics industry by far are the main drivers in China,” says Gemma. “The automotive industry is always a big driver of automation. Installations went from roughly 14,000 to 21,000 units in 2014. But the electronics industry has already started to automate its assembly processes. Robot sales to the electronics industry in China alone rose from roughly 6,500 in 2013 to 16,000 in 2014, so it more than doubled.”

Swiss-based robot manufacturer ABB, Japanese robot makers FANUC, Kawasaki, Nachi, and Yaskawa Motoman, and German-based KUKA still account for the majority of industrial robot sales. But Gemma notes that Chinese robot manufacturers will play an increasingly larger role in automation growth within their country. You can see the significant increase in Chinese robot suppliers from 2013 to 2014 as indicated by the shaded areas in the accompanying bar chart.

“Only a few years ago there was less than a handful of manufacturers,” says Gemma. “The industry is getting a real stronghold in China by equipping itself to be a producer of robots, as well as a consumer of robots.”

Dan Kara is Research Director, Robotics, for ABI Research headquartered in Oyster Bay, New York. He sees the growth in industrial robot installations in Asia, and primarily China, as a major development with long-range implications.

“The large, traditional robot vendors have been in China for a long time. Many of them have offices there,” says Kara. “But now we’re seeing other political and social drivers. The Chinese government is getting involved with issues related to salaries and workforce flexibility. The country as a whole has decided to focus on automation as a way to create an innovation economy as opposed to just a low-cost manufacturing economy. I think this is a massive story.”

He sees the applications in this market expanding as well, from large assemblies in the automotive and white goods industries, to more electronics manufacturing for fine assembly, and even testing.

“One of the areas we see a lot of growth is in the electronics manufacturing services marketplace,” says Kara, referring to large, global contract manufacturers such as Foxconn, Jabil, and Flextronics. “They are trying to automate as much as possible wherever they can.”

China’s robot revolution is gaining ground with Chinese robot manufacturers such as Shanghai SIASUN Robot & Automation, Dongguan Start To Sail Industrial Robots, Anhui Efort Intelligent Equipment, GSK CNC Equipment, Shanghai STEP Robot, and Estun Robotics.

Frank Tobe, a long-time robotics industry analyst and Editor/Publisher of The Robot Report, has identified more than 50 Chinese producers of industrial robots. He has pinpointed a total of 194 Chinese companies involved in robotics, including robot integrators and suppliers of ancillary services, sensors, and components rounding out the mix.

“I see China expanding everywhere you look, particularly in Silicon Valley,” says Tobe, who resides in California. “You have think tanks for Baidu, Alibaba, JD.com, and LeEco in Silicon Valley,” noting a recent trend in venture capital spending.

Tobe is also Cofounder of ROBO Global, the first Robotics and Automation Index ETF (Nasdaq: ROBO). We introduced you to Tobe and his benchmark index, formerly called ROBO-STOX, in our 2014 market forecast article.

He considers artificial intelligence the big news in automation. It’s about the software, the algorithms. Toyota’s billion-dollar investment in AI certainly raised eyebrows.

Industry 4.0 and the Smart Factory

Many recent advancements in automation and robotics have an AI component. Industry 4.0 or the Industrial Internet of Things (IIoT) is no longer an abstract theory. Advanced sensors, sophisticated software, and autonomous actuators are raising the factory’s intelligence. The smart factory of the future is already here.

IFR’s President says Industry 4.0 was the big news and prevailing theme at HANNOVER MESSE, a four-day trade fair for industrial technology in April. The fair’s showstoppers were autonomous, intelligent and self-learning. Watch them in action.

Industry 4.0 will also be one of the highlights at AUTOMATICA in Munich this June. IFR is an event co-sponsor. Gemma says this is a hot topic among the automation and robotics community. In some respects, it’s familiar territory.

“What is interesting is that the automation industry has been on the edge of that kind of communication capability on the plant floor for some time now, although we didn’t call it that for several years,” says Gemma. “Having communication across devices and gathering information and feeding it back to the whole system, and then managing equipment based on that information. That is what a lot of Industry 4.0 or the Industrial Internet of Things is capturing. So robotics and automation have been ahead of that curve for some time.

“Now, you can get this information and use it across other plants, and also your suppliers and customers,” he continues. “Now through industry 4.0 or IIoT, it’s possible to connect right through the value chain. That’s the big news going forward.”

Internet of Robotic Things (IoRT)

Last fall, ABI Research’s Kara introduced a new concept, the Internet of Robotic Things (IoRT). He distinguishes it from IoT, which largely focuses on using connected devices with simple, passive sensors to monitor and optimize systems. IoRT, on the other hand, uses devices to fuse sensor data from a variety of sources, uses “intelligence” to determine a best course of action, and then acts to control or manipulate objects in the physical world, while in some cases, moving through that world.

“We’re talking about robotic devices that actuate dynamically, that have some degree of movement in the physical world and with some degree of autonomy,” explains Kara. “That combination of sensing, communication, processing, plus actuation takes IoT to a completely different level. It can improve robotic manipulation and grasping, navigation and localization, and path planning.

requires sensing, communication, processing and actuation to take the smart factory to new levels of intelligence. (Courtesy of ABI Research)")

“You can see how these uber-sensors, which is really what a robot would be as a highly sensored object that can move through the physical world and manipulate it, can now act as an edge device in ways that static devices are simply not capable,” he continues. “The robot is able to sense conditions, collect data, and understand it. Then it can feed it to the back-end, so decisions on how to act can be made in real time.”

Real-time intelligence and the ability to immediately act upon it is why Kara was particularly intrigued by a recent strategic partnership.

Strategic Partnerships for Connectivity

Some of the biggest collaborations are taking place in the cloud. FANUC, Cisco, Rockwell and Preferred Networks entered a strategic partnership to develop the Fanuc Intelligent Edge Link and Drive (FIELD) platform.

“What I liked is that it wasn’t just an announcement of a partnership about R&D or a vision announcement,” says Kara. “They have a number of installations, some of which have been running a year and a half or longer where different CNC machines and robots are working together. They’re actually able to capture that data and do some deep analysis on it. To show that they are able to train their systems, so they can go to a deeper level of understanding as opposed to just that top-level analysis where a lot of IoT stuff is limited to at this time.”

The FIELD system is an extension of FANUC’s ZDT connected robots project that helps manufacturers reduce production downtime. Kara says FIELD represents a big step towards IoRT.

Chinese information and communications technology (ICT) giant Huawei partnered with KUKA to develop smart manufacturing solutions for industrial markets in Europe and China.

") “Huawei is well known for smart phones and electronic devices, but it also has its own division for enterprise solutions, or business services,” says Gemma. “That’s a valuable partner for KUKA. It gives us more of a diversified portfolio for our customer base. This agreement and collaboration with Huawei in the areas of cloud computing, big data, mobile technology, and industrial robots will help manufacturing customers transform and perhaps embrace smart manufacturing through us as a service.”

“Huawei is well known for smart phones and electronic devices, but it also has its own division for enterprise solutions, or business services,” says Gemma. “That’s a valuable partner for KUKA. It gives us more of a diversified portfolio for our customer base. This agreement and collaboration with Huawei in the areas of cloud computing, big data, mobile technology, and industrial robots will help manufacturing customers transform and perhaps embrace smart manufacturing through us as a service.”

KUKA’s mobile collaborative robot plays an integral role in this vision. The KMR iiwa autonomous mobile robotic platform and its manual rolling version, the flexFELLOW, were both featured in a mini smart factory demonstration at the HANNOVER MESSE fair.

For Diversity and Market Penetration

Gemma says KUKA’s strategic partnerships and acquisitions have positioned the company for more diversification and a stronger presence in general industry.

“General industry is where the market is growing strongly, so for us, entire fields of robot-based automation is on the horizon,” says Gemma. “It’s not just electronics. It’s medical, it’s pharmaceutical, it’s aerospace, and some of the other areas we’re working in to position us to be able to provide even more services to that client base.”

Other collaborations such as the joint venture between Yaskawa Motoman and Chinese home appliance maker Midea harbor hopes of bringing traditional manufacturers into the future.

Speaking of the future, as we headed to press, news broke of Midea’s $5 billion bid for KUKA AG, the German parent company of Michigan-based KUKA Robotics Corporation. Stay tuned, we’ll have to see how this plays out. (Told you the business of automation moves fast!)

“Because the smart factory is about interconnected capabilities, to be able to support that, you must have more diversified capabilities and be able to work across the globe in various markets,” says Gemma. “If you’re too centralized in an area or in a technology, you might not be able to support the market the way it’s headed. All of the companies are trying to better position themselves to have a broader perspective and be able to support that type of service across the globe. I believe that’s the major driver behind this collaboration between companies, or the merger and acquisition strategies.”

Mergers and Acquisitions

M&A activity in robotics and automation has grabbed big headlines of late, and involved some even bigger names. Amazon, Google, and iRobot are just a few.

Gemma uses Teradyne’s acquisition of collaborative robot manufacturer Universal Robots as an example of the convergence taking place in the industry.

“Teradyne certainly had a play in a particular piece of the electronics industry prior to Universal Robots, but they were missing a component to be fully functional to the marketplace,” says Gemma. “The acquisition makes sense for them to be able to provide the full service that their customers will be looking for now and in the future.”

“Universal Robots was expanding anyway,” says Kara, “but now they have a world-class company behind them and Teradyne’s contacts as the largest supplier of automated test equipment in the world. Teradyne is on a first name basis with all of those electronics manufacturing service people. That’s important.

“Also, for the investment community, it was a signal that you can have a robotics startup and get it acquired fairly quickly,” he adds.

Others are torn over the absorption of Universal Robots. ROBO Global ETF’s cofounder Tobe says this was one of the companies on his IPO watch list.

“I try to follow every company in the robotics industry,” says Tobe. “I put them in a database and those that are interesting to me and which I think have a chance at success, I try and look at their websites and press releases on a regular basis. I’m hoping that these companies will go public.”

Universal Robots was already on his radar two years ago when we first met Tobe. He was hoping the cobot manufacturer would hit 5,000 installed units by 2014-end and then throw their hat in the ring. But Teradyne had other plans.

“Universal Robots was one of my IPO watch list companies that I was annoyed got acquired,” says Tobe. “But that happens. We added Teradyne to the index.”

He says he still has his eye on the prize. In February, Universal Robots reported 2015 revenue of $61.44 million, a 91% increase over 2014.

“As Universal Robots becomes a bigger percentage of Teradyne’s revenue stream, which it very well might, then Teradyne becomes more interesting,” says Tobe. “The same thing with Omron (Omron Corporation acquired Adept Technology in 2015). Adept is a very small piece, but Omron is already in the index, so it might become more interesting because of Adept.”

To be a part of the index, Tobe says companies must have a market value of at least $200 million, a trading volume of greater than $1 million a day, and at least 25 percent involvement in the robotics industry.

“My IPO watch list keeps getting bombed by acquisitions. April was a big month for robotics investments for some reason. I worry about the level of acquisitions, because it takes away from the stock market and from people sharing in the activity. On the other hand, this is the year we start equity crowdfunding. To me, that’s a game changer. It’s like an IPO, but not.”

ABI Research’s Kara sees Amazon’s acquisition of KIVA Systems as a competitive advantage.

“Amazon bet on robotics. They bought KIVA for $775 million in 2012. The cost of fulfillment operations was just too much and it wasn’t sustainable, so they started focusing on automation. Now they’re getting that cost of fulfillment down. It’s no longer a cost center. It’s a strategic advantage that Amazon bought this particular company and is using robotics in this particular way. They are able to provide same-day delivery or two-day delivery because they’ve automated using robotics.”

“That’s a competitive differentiator,” adds Kara. “Robotics is now a strategic advantage.”

KUKA’s Gemma sees all of this M&A activity as a good thing, as a sign of expansion.

“It means the industry is growing. The needs of the market are growing and we all need to position ourselves to support the markets. In all the cases that I know of, the acquisitions have helped to make the existing companies stronger. It’s positioning for growth.”

Collaborative Robotics and SMEs

Dramatic growth will come from the 90 percent of the market for robotics that isn’t yet automated. These are the small and midsized enterprises across the globe, the largest sector of the manufacturing base. Find out How SMEs in the Know Win with Automation.

“Small to midsized companies are now looking to engage in using automation,” says Gemma. “Ease of use will dramatically increase the opportunity for them to use robots. In the electronics industry their life cycles tend to be fairly short, so they want something they can quickly interface with, so ease of use will be a dramatic push. Our whole industry understands this is the trend going forward.”

No other sector of the robotics industry has pushed the envelope for ease of use more than human-robot collaboration and the unique robots that occupy this space. Beyond ease of use, collaborative robotics will play a vital role in the proliferation of automation among SMEs. The new breed of cageless robots is knocking down all kinds of barriers.

“With traditional robots, those robots had to do either all or nothing,” explains Gemma. “They did all the work because you couldn’t have a human in the space. Or they did nothing because it had to be done by a human. That’s one of the big differences between collaborative robots today. It’s allowing for part of the process to be done by a robot and part of the process can be done by a human. Now the robot can be right alongside the person and do some final assembly and then the person does the inspection.

“There’s a cost benefit that didn’t exist in the past,” he says. “You needed to have a safety structure around the robot and different analysis capabilities to be able to support a piece of equipment like that on the factory floor. For a small to medium-sized company, it was cost prohibitive. With the advent of collaborative robots that are not only easier to use, but also easier to implement, and not requiring the same safety environment around them, has made it much more cost effective for companies to implement.”

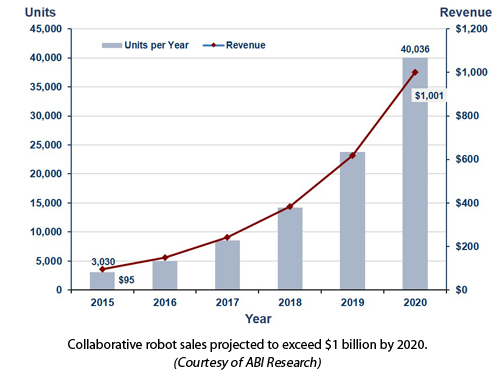

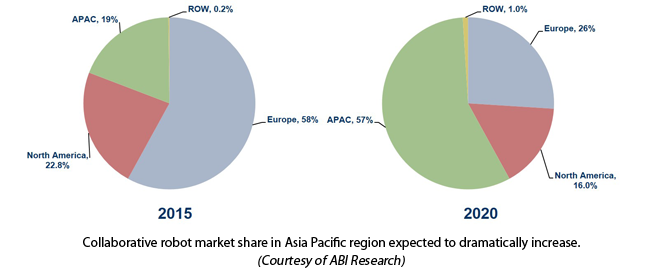

In a study conducted in 2015, ABI Research estimates that the collaborative robots market will exceed $1 billion by 2020. The study indicates that the market share for collaborative robots in the Asia Pacific (APAC) region will dramatically increase from 19 percent in 2015 to 57 percent by 2020. This is in line with the projected growth of robotics implementation in Asia, and particularly China.

Gemma sees great potential for collaborative robots on the automotive assembly side where cockpit electronics and seating is installed. Where it used to be “all or nothing,” collaborative robots will play a huge role.

Mobile Robotics

Gemma says mobile robots will also be an important tool in the smart manufacturing movement. They were prevalent at the Hannover trade fair and he expects to see more at AUTOMATICA.

“The industry is showing more robots on mobile platforms moving from process to process,” says Gemma. “Industries like plastics, machine tool, and drug discovery have the ability to take advantage of this technology. There are multiple areas where in the past it was very difficult to have automation processes, where now given the dynamics of mobile platforms, could bring it closer to their industry and their environments.”

“Mobility is the big new thing,” says Tobe. “Bin picking is finally working. Now, if you want to move a bin from here to there, you don’t want a conveyor system. You don’t want a positioning system. These things cost money and they are fixtures. You don’t want a fixture in your warehouse. You want mobility. Whether it’s Adept or Swisslog, or any company that makes mobility devices, that’s the coming trend in my opinion.”

Kara also noted a lot of investments in mobile service robots for areas such as e-commerce logistics, the hospitality industry, and in warehousing and manufacturing.

“Robots can now navigate indoors and outdoors with high precision in people’s environments, or unstructured environments,” says Kara. “They can move through hospitals, through hotels, through warehouse and distribution centers.”

Mobile robots are sure to straddle the lines between the industrial and service robotics sectors.

UAVs, Healthcare

Outside of the industrial sector, Kara notes high volumes of investment in commercial unmanned vehicles. He says 2015 alone showed massive investment.

“Last year, in the private sector, robotics investments were around $1.6 billion, up from about $350 million the year before. So it’s three times the size, at least. You see big companies like Qualcomm and Intel, as well as large venture companies putting money into that space. No doubt there is big money in industries such as oil and gas, agriculture, and mining. These are massive marketplaces that are done outdoors. Just one percent increase in profitability is huge.”

Kara says healthcare is another booming area for robotics investment.

“These weren’t seed rounds or A rounds” says Kara. “These were late rounds of a lot of money. We’re talking $60 or $70 million. That’s just the nature of healthcare robotics, particularly when you get into surgical systems.”

One of last year’s most notable investments was an eye-opening $150 million for Auris Surgical Robotics, a Bay Area startup developing a microsurgical robot for cataract removal. And just last month, Auris announced an agreement to acquire Hansen Medical, a leader in intravascular robotics.

Investment Boom or Bust

Investment funding in robotics is booming. CB Insights reports a 115 percent increase in 2015. Beyond Auris, notable recipients include Restoration Robotics, Rethink Robotics, Liquid Robotics, Aethon and Jibo.

ABI Research’s Kara warns that not everything is moving to the upper right. Every week another study surfaces, by another research firm on another sector of the robotics industry, many with conflicting and overinflated stats. He offers the mobile telepresence market as an example of a sector he thinks has been overinflated.

“Robotics has become very hot, so you’ve seen a lot of research companies pop up ipso facto,” says Kara. “Everybody has an opinion. We have numbers.”

When conducting much of his research, Kara goes directly to the sources – the manufacturers and users, and the investors. Kara himself has been in the robotics industry for 12 years. Prior to ABI Research, he was Chief Research Officer for automation and robotics research firm Myria RAS. Kara was also President of Robotics Trends media firm for seven years, and founder of RoboBusiness.

“I have a lot of contacts in the VC community,” says Kara. “They are betting with their dollars. They are not easily fooled. They don’t believe the hype that they see.”

The media has been known to contribute to the hyperbole. Take all the press and speculation over Google’s robotics acquisitions in 2013. Kara puts the Google’s buying spree, a reported eight companies, into perspective.

“One company (Holomni) just made casters and it’s a single person. Two of the companies (Bot & Dolly and Autofuss) had the same address and the same CEO, so it’s essentially the same company. And there’s another one (Meka Robotics and Redwood Robotics) that had the same address and same CEO. So out of these eight companies, you’re really talking about four.”

One of Google’s notable four, Boston Dynamics, is now up for sale. Speculation over prospective buyers is almost as feverish as the conjecture surrounding the reasons for its purchase it in the first place. Robot Report’s Tobe thinks a hedge fund will probably buy Boston Dynamics, similar to iRobot selling its defense and security robotics division to Arlington Capital Partners.

Kara describes two major categories of investors. One is the pure private equity venture capitalists. These are the classic VCs whose primary source of income stems from investment payoffs. The other category is made up of a variety of organizations with vested interests.

“They can be national entities, so for example one of the major investors in Savioke (mobile hospitality robots) was Singapore,” says Kara. “The Singapore government has its own investment wing. That exists all throughout the world. There’s also big companies like Google, Qualcomm, Oracle, and Intel that all have investment arms. iRobot is another example.”

iRobot Ventures, the company’s VC arm, is part of a group that reportedly invested in 6 River Systems to develop warehouse fulfillment robots.

For his research into the robotics exoskeleton market, expected to reach $1.8 billion in 2025, Kara went right to the sources. He quickly noticed an interesting trend emerging.

“When I looked at this marketplace, it’s basically given over to rehabilitative and therapeutics,” says Kara. “That’s where the money was to get research dollars for investment. There’s also money coming from the DOD. There’s a huge social and moral imperative to help these folks. But I started noticing that all the major manufacturers had made a pivot to focus on manufacturing or on areas like construction. They know this marketplace is much larger.

“To use these technologies in areas such as manufacturing, or in construction, or warehouse operations, or in areas like airports for lifting bags, you will see that these guys all now have a business line that focuses on the commercial sector.”

Kara also finds development in soft robotics interesting. Combining soft robotics and wearable robotic exoskeleton technologies, SRI International made news on both fronts with its Superflex spin-off.

“The announcement by SRI about the soft robotics exoskeleton, that’s a big deal,” says Kara. “That’s a heavy hitter.”

More and more heavy hitters are betting on the veracity of robotics and automation. There are more hits than errors. The same goes for the precipitous debate over robots stealing our jobs. Just like the other three before it, this Fourth Industrial Revolution will ultimately create jobs. Robots will transform industries, foster new economies, and free humans from the drudgery of manual processes. Free to do what we do best – think, imagine, create. That’s our business.

")

")